Your brain automatically resets to new income levels through a natural process called hedonic adaptation while small lifestyle changes consume raises. Learn why this disappointment is normal psychology.

Why your brain treats every raise like it never happened

Your brain automatically adjusts its baseline expectations when your income increases through hedonic adaptation, making the temporary satisfaction from a raise quickly become your new normal. Within few weeks, your reward system recalibrates what feels satisfying, treating yesterday’s exciting income boost as today’s ordinary expectation.

Think of your brain’s satisfaction system like a thermostat that constantly resets itself to whatever temperature it experiences most often. When you get a raise, there’s an initial rush of excitement and relief. Finally, you can breathe easier about money. But your brain doesn’t maintain that elevated feeling of gratitude or financial security.

Here’s what actually happens in your reward system: the dopamine hit you get from seeing a bigger paycheck is based on the contrast between your old income and your new one. But dopamine responds to change, not absolute amounts. Within a few weeks, your brain stops comparing your current paycheck to your old one. It starts treating your new income level as the baseline for normal.

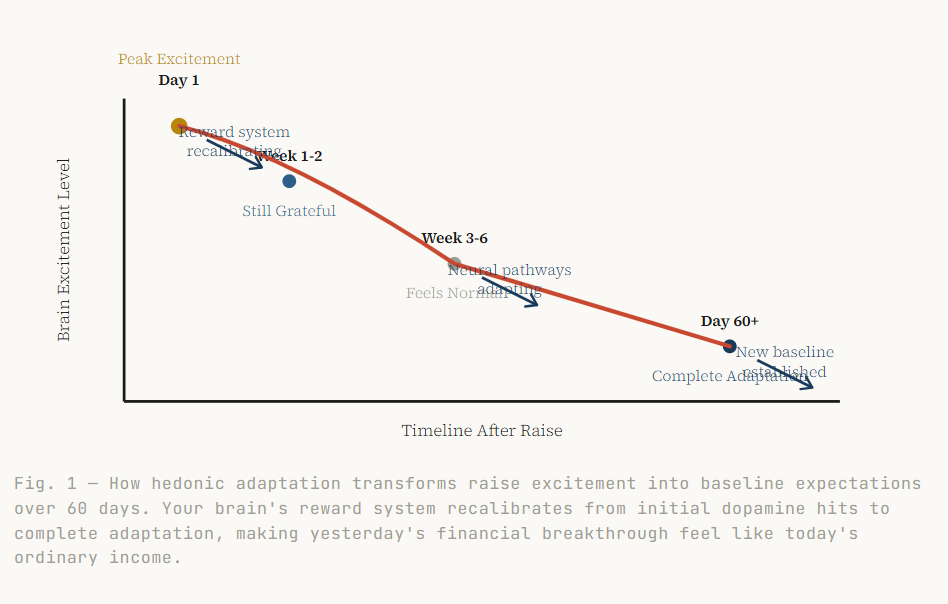

This process typically takes few days to months. The timeline depends on how significant the raise feels relative to your previous income. During this time, your brain is literally rewiring its expectations. The neural pathways that once fired with excitement when you thought about your salary gradually quiet down as the new amount becomes familiar.

By the time a couple months have passed, your brain has established this higher income as your new reference point for “normal.” This means it no longer generates feelings of excitement, gratitude, or financial relief. It’s not that you’ve become spoiled or ungrateful. Your reward system has simply done what it’s designed to do: adapt to your current circumstances so you can focus on detecting new changes in your environment.

Your brain measures financial progress by comparing today to yesterday, not by comparing your current situation to an objective standard of wealth.

The 60-day reset timer in your reward system

The timeline for hedonic adaptation isn’t random. It follows a predictable pattern that researchers have observed across different types of positive life changes. In the weeks after your raise, you’ll likely feel genuine excitement every time you think about your new salary or see your paycheck. The contrast with your previous financial situation feels vivid and meaningful.

Between weeks 2-8, this excitement gradually fades as your brain processes the new income level as increasingly normal. By day 60, most people report feeling completely adapted to their raise. It generates no more emotional satisfaction than their previous salary once did.

How yesterday’s luxury becomes today’s baseline necessity

Once your brain adapts to higher income, it doesn’t just feel neutral about the extra money. It actually starts treating spending at your new level as necessary rather than optional. The restaurant meals that felt like special treats during your first weeks of higher pay begin to feel like normal dinner choices.

This shift from “luxury” to “necessity” happens because your brain constantly updates its internal model of what constitutes reasonable spending for someone in your position. When you know you can afford slightly better options, choosing cheaper alternatives starts to feel artificially restrictive rather than naturally frugal.

How lifestyle inflation eats your raise without you noticing

Lifestyle inflation occurs through hundreds of unconscious micro-decisions like slightly better coffee, modest restaurant upgrades, and small convenience purchases that each seem reasonable but collectively consume your entire raise. These spending escalations happen automatically as your brain adjusts to what feels appropriate for your new income level.

While your brain is busy adapting to your new income baseline, something else is happening to your actual money. You’re spending it in ways that feel completely reasonable but add up to consume your entire raise. This isn’t about making obviously expensive purchases or deliberately upgrading your lifestyle. It’s about dozens of small daily choices that shift slightly upward.

Here’s how it typically unfolds: you might start buying coffee from a slightly nicer place. After all, you can afford it now. Instead of the $2 coffee, you get the $4 one. It’s just two dollars, and you work hard — you deserve it. Then when you’re grocery shopping, you find yourself choosing the organic option more often. You grab that pre-made salad instead of making lunch. Each decision feels minor and justified.

The same pattern emerges in dozens of other areas. You might park in paid spots more often instead of walking from free parking. You order delivery instead of picking up food. You choose the slightly nicer hotel when traveling. You replace things a little sooner than you used to. None of these feel like major lifestyle changes. Individually they’re all affordable with your new income.

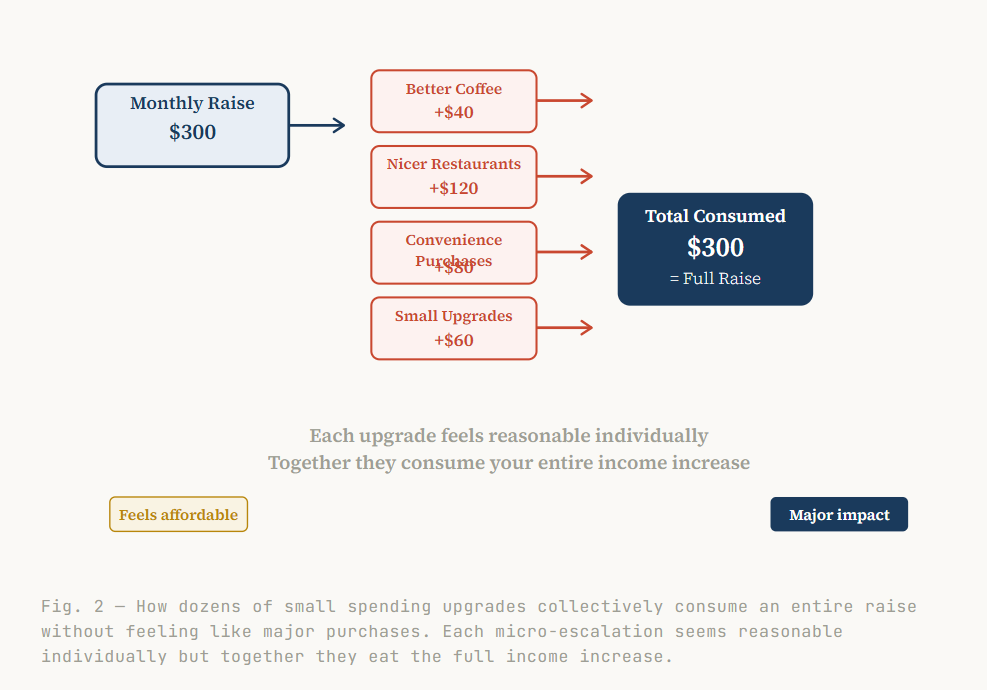

But when you add up all these micro-escalations, you’ve often consumed your entire net raise increase. An extra $40 per month on coffee, $80 on more convenient food choices, $60 on small comfort upgrades, $120 on restaurant spending — all without creating any sense of living dramatically differently than before.

Lifestyle inflation succeeds by feeling completely reasonable in each individual moment while being financially significant in aggregate.

The coffee-to-convenience spending escalation pattern

The progression from small indulgences to significant budget impact follows a predictable pattern. It starts with low-stakes decisions like better coffee or lunch, where the price difference feels negligible compared to your raise. These choices establish a new spending baseline that makes slightly bigger upgrades feel equally reasonable.

Once you’re comfortable spending $4 on coffee instead of $2, spending $12 on lunch instead of $8 doesn’t feel dramatic. The decision-making threshold has shifted. Each new spending level becomes the foundation for the next small escalation.

Why small upgrades feel reasonable but add up to your entire raise

Your brain evaluates each spending decision against your new income level, not against your cumulative spending changes. When you’re deciding whether to spend an extra $3 on convenience, your brain compares that $3 to your total monthly income, where it feels insignificant.

But you’re not making just one $3 decision per month. You’re making dozens of small upgrade choices across different spending categories. Your brain doesn’t naturally track these cumulative impacts because each individual decision genuinely is affordable and reasonable given your higher income.

Why this happens to everyone regardless of income level

This experience is completely normal human psychology, not a sign that you’re bad with money or ungrateful. Your brain is designed to quickly adapt to improvements and establish new baselines, which explains why people earning $50k and people earning $500k report similar patterns of temporary satisfaction followed by return to baseline financial stress.

This pattern of disappointment after income increases affects virtually everyone who receives raises. The mechanism of hedonic adaptation doesn’t care how much money you make. It operates the same way whether you’re going from $40k to $45k or from $200k to $240k.

Research on lottery winners provides an extreme example of this principle. People who win millions of dollars report being significantly happier than average for about six months. After that, their self-reported happiness levels return to roughly where they were before winning. If suddenly becoming a millionaire doesn’t create lasting satisfaction, a 10% or 20% salary increase certainly won’t either.

This pattern repeats at every income level because your brain doesn’t measure wealth in absolute terms. It measures relative improvement and relative status. Someone earning $300k can feel just as financially stressed as someone earning $60k. Both of their brains have adapted to their respective income levels as normal and are focused on the gap between their current situation and their aspirations.

Your financial stress level is determined by the gap between your income and your adapted expectations, not by your absolute income amount.

What to do when you realize your raise already feels like nothing

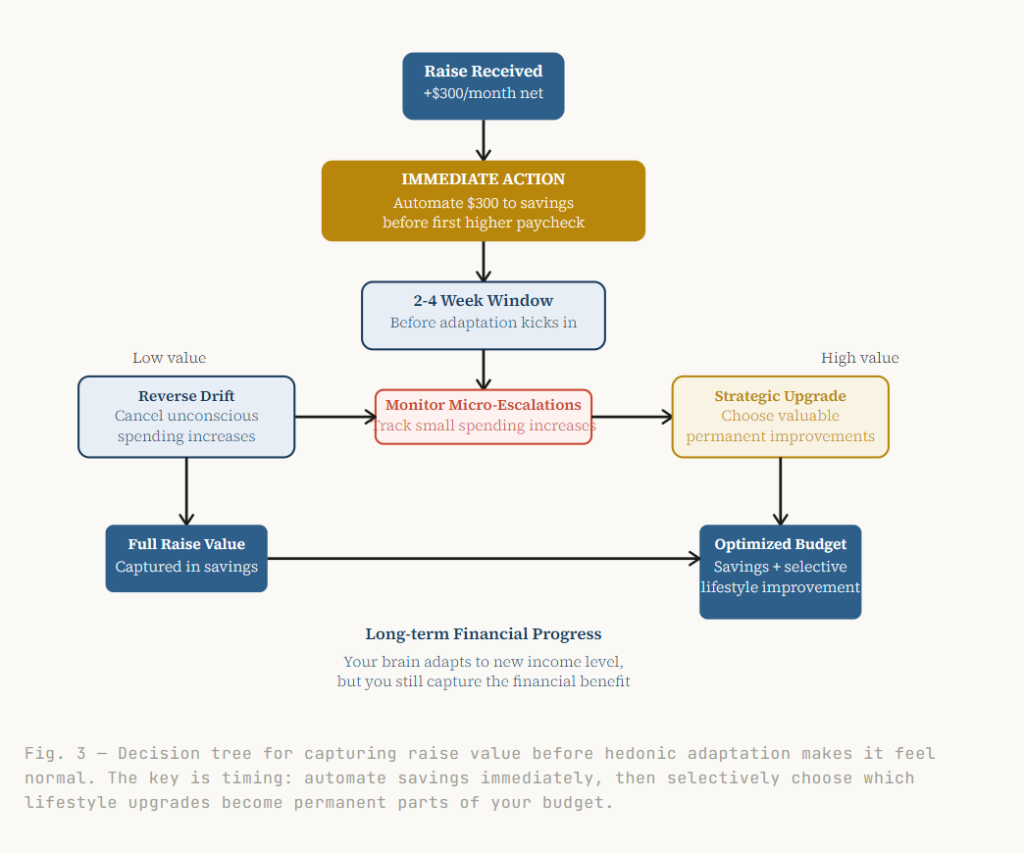

The solution isn’t fighting your brain’s natural adaptation process, but working with it by creating systems that capture value before adjustment happens. This means immediately automating savings with your net raise amount and being strategically selective about which lifestyle upgrades you allow to become permanent.

Once you understand that hedonic adaptation and lifestyle inflation are inevitable, you can design systems that work with these psychological realities rather than against them. The key is timing: you need to capture the value from your raise before your brain adapts and before spending patterns escalate to consume it.

The most effective approach is to automate savings or investment increases immediately when you get a raise. Do this ideally before you receive your first higher paycheck. If your net raise amount is $300 per month, set up an automatic transfer of $300 to savings or retirement accounts. This captures the full financial benefit before lifestyle inflation has a chance to absorb it through micro-escalations.

But you don’t have to live exactly the same lifestyle forever. Instead of letting lifestyle inflation happen unconsciously across dozens of categories, choose deliberately which upgrades are worth making permanent parts of your budget. Maybe you decide that better coffee is genuinely worth $40 per month to you. But you’re not willing to permanently upgrade restaurant spending or convenience purchases.

Financial progress comes from capturing raise value before your brain adapts to expect it, not from fighting adaptation after it’s already happened.

Interrupt the micro-escalation cycle before it becomes automatic

The window for intervention is narrow. You have roughly 2-4 weeks after getting a raise before new spending patterns become psychologically entrenched. During this period, pay attention to the small daily choices where you’re starting to spend slightly more than usual. Decide consciously which ones you want to keep versus which ones you want to reverse.

Create a simple rule for yourself: any new recurring expense that didn’t exist before your raise gets evaluated after one month. Ask yourself whether this spending genuinely improves your life enough to be worth the permanent budget impact, or whether it just happened unconsciously as part of lifestyle drift.

Set up systems that work with your brain’s adaptation patterns

Since you know your brain will adapt to higher income and start treating it as normal, design your financial systems to take advantage of this predictable psychology. Set up automatic savings increases that match your raise. Even after you adapt to your new income level, you’re still capturing the financial benefit.

You can also use adaptation to your advantage by automating lifestyle upgrades you genuinely value. If you decide that grocery delivery is worth $50 per month to you, automate that expense. You don’t have to repeatedly decide whether you can afford it — you’ve already allocated it as part of your post-raise budget.

Frequently asked questions

How long does it take to stop feeling excited about a raise?

Most people feel the excitement and relief from a raise fade within 14-60 days as their brain recalibrates to the new income level through hedonic adaptation. The exact timeline depends on how significant the raise feels relative to your previous income, but by two months, most people report feeling completely adapted to their higher salary.

Is it normal to feel exactly the same after getting more money?

Yes, feeling financially unchanged after a raise is completely normal human psychology, not personal failure. Your brain is designed to quickly adapt to improvements and establish new baselines. The temporary satisfaction from income increases naturally fades as your reward system recalibrates to treat the higher income as ordinary rather than exciting.

Why do I spend more money when I earn more without meaning to?

Lifestyle inflation happens through unconscious micro-decisions where you choose slightly better options across dozens of daily spending categories. Each choice feels reasonable given your higher income. Collectively these small upgrades consume your entire raise without feeling like major lifestyle changes.

Does everyone experience this disappointment with salary increases?

Yes, hedonic adaptation affects people at all income levels — from those earning $40k to those earning $400k. The mechanism doesn’t depend on absolute income amounts but on the psychological process of adapting to improvements. This explains why even lottery winners return to baseline happiness levels within months.

Can you prevent lifestyle inflation from happening automatically?

You can’t prevent the psychological tendency entirely. But you can manage it by immediately automating savings with your raise amount and consciously choosing which lifestyle upgrades to make permanent. The key is intervening within 2-4 weeks before new spending patterns become psychologically entrenched.

Why does a 20% raise feel like nothing after a few months?

Your brain measures satisfaction based on recent changes rather than absolute amounts. After a few months, your reward system has adapted to the higher income as your new baseline normal. It no longer generates feelings of excitement or financial relief when compared to your previous salary.

Is there something wrong with me if I still feel broke after a promotion?

Nothing is wrong with you — feeling financially stretched despite earning more is universal human psychology. Your brain automatically adjusts its baseline expectations to match your new income level. Meanwhile, lifestyle inflation often absorbs the extra money, leaving you feeling exactly as financially constrained as before.

How do some people seem satisfied with their raises when I’m not?

People who seem satisfied with raises often capture the financial value through immediate automation before lifestyle inflation occurs. They might also still be within the first few months before hedonic adaptation is complete. The satisfaction isn’t about being different psychologically — it’s about timing and systems that work with brain adaptation rather than against it.

The Bottom Line

Getting a raise that doesn’t make you feel richer isn’t a personal failing — it’s your brain working exactly as designed. Through hedonic adaptation, your reward system automatically recalibrates to treat higher income as normal within weeks. Meanwhile, lifestyle inflation quietly absorbs the extra money through countless small, reasonable-feeling spending decisions.

This experience is so universal that it affects people at every income level, from entry-level salaries to executive compensation. Understanding this pattern gives you power over it. Instead of fighting your brain’s natural tendency to adapt and escalate spending, you can work with these psychological realities. Capture raise value immediately through automated savings and make conscious choices about lifestyle upgrades rather than letting them happen unconsciously.

The goal isn’t to never enjoy the benefits of earning more — it’s to be strategic about which benefits you choose and to secure your financial progress before your brain adapts to expect it.